Ford’s US sales fell despite a nationwide rise of 9.5%, while rival GM improved thanks to fleet sales

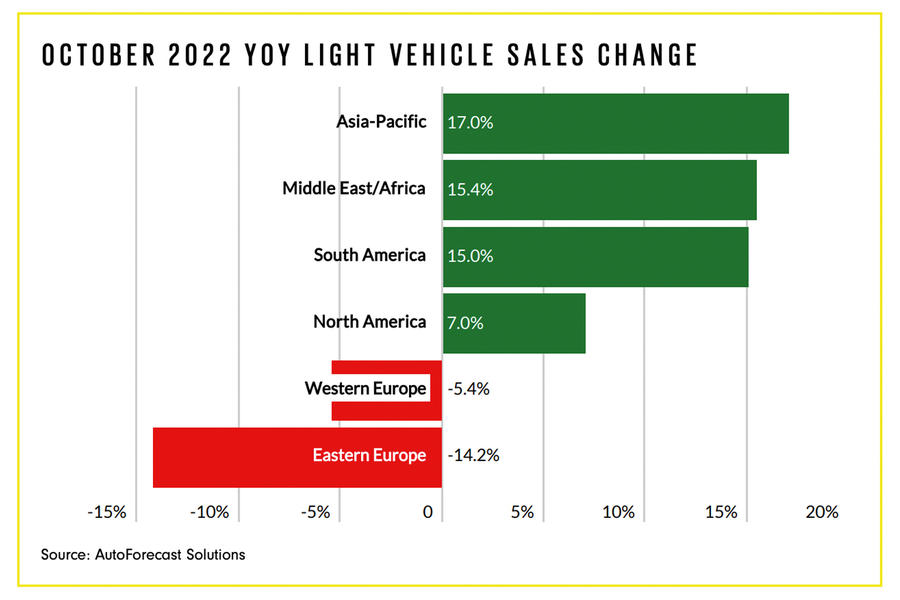

Europe’s poor figures slump further, contrasting the Americas’ strong performance

Buyers are getting worried about the economy and where things will be as the holiday season begins and the new year approaches.

Extended threats of a recession through price inflation and the constant barrage of talking heads warning of the “R” word may have generated the belief of its arrival with or without the actuality of it. Believing that a recession is near has the same result as the official announcement of the downturn: consumers decide to save money rather than spend it. And global national banks increasing interest rates have compounded the slowdown.

For years, the automotive industry has focused on the pent-up demand of buyers who did not buy a new vehicle during the COVID shutdown and could not find a vehicle in the post-shutdown inventory shortage. These buyers normally would have shifted to used vehicles but the shortage of pre-owned vehicles has raised prices to record levels. Combining high vehicle prices and short supply moved potential buyers out of the market. Maintaining old vehicles has become the norm, as can be measured by the continued rise in the average age of vehicles on the road. In the US, the average vehicle has been in use for well over 12 years.

To put that average age in perspective, more than 13 million vehicles will be sold in the US in 2022 on top of the 186 million vehicles sold in the prior 12 years. Today, there are about 280 million vehicles in use in the US, which means a substantial number of vehicles on the road today were produced more than two decades ago. The reliability of cars and trucks produced this century is so good that owners do not need to upgrade when these vehicles hit 100,000 miles, or even 200,000 miles. Knowledge of this has permeated the market, moving more buyers out of it and allowing them to save the average transaction price of nearly US$50,000 (£41,998) for a new vehicle or US$33,000 (£27,712) for a used one. Pent-up demand isn’t satiated as much because these buyers simply walked away from the market.

This story is an extract from the November 2022 issue of AutoForecast Solutions’ monthly report. Click here to download the full report, or to catch up on previous months

Sales in China during September grew over the year prior, but not by as much as anticipated. Each of the past four months has surpassed 2021 numbers and September’s 9.3% growth would be the envy of most markets around the world. Coming off the fourth straight year of reduced sales, positive signs of any kind are welcome. However, 2022 is still expected to be 3% below even the 2020 level and more than 21% below the peak year of 2017.

The United Kingdom is slowly recovering from the COVID-era downturn and this year won’t demonstrate that recovery. August and September recorded gains, joining January and February as the only months not in the red. Even with an expected positive fourth quarter, this year will still lag behind 2021 by 6%. Economic troubles inside the United Kingdom and around the world will keep the region from growing too quickly and most of this year’s losses will be recovered, but still well below pre-COVID levels.

Sales in the EU are doing no better. Last year, the EU slipped 2.4% from 2020’s sub-10 million total, itself down 24.5% from 2019. This dismal track record continues in 2022. When all of the numbers are in, this year will fall below 8.7 million units of light vehicles, an additional 10.8% lower than last year’s terrible showing. A slight recovery in 2023 won’t push sales volumes back over nine million units and the region won’t return to 10 million units before 2025.

US light vehicle sales rose 9.5% in September, powered by a few major players. With slightly improving inventory levels, Toyota, Hyundai, Subaru and General Motors found more buyers last month than they had a year prior, while sales at Ford, Stellantis and Nissan fell. GM’s improvement was thanks, in large part, to increased sales to fleets as retail sales lagged behind the overall market.

Sales in Canada were down 9.6% in September, which was as expected. Inventory shortages remain the biggest stumbling block to market growth and no remedy is on the immediate horizon. With just one quarter left in the year, the outlook for 2022 remains at 1.5 million units, followed next year by marginal growth of just 6%, taking the market above 1.6 million vehicles.

The 4.8% rise in sales in Mexico was right on forecast for September, following last month’s sales growth. Again, two months do not make a trend, but this does follow the slowing inflation in the country as a positive sign for future growth. Light vehicle sales are still on pace for 1.05 million units this year.

South America got a boost, as usual, from Brazil. The region’s largest market saw vehicle sales crater last September, setting the market for substantial growth last month. Rising nearly 27% looks great on paper, until it is pointed out that September 2021 was down over 28% from the prior year, which in turn was down nearly 11% from 2019. Third quarter economic growth in Brazil was very good just ahead of the presidential election and this is expected to continue for the rest of the year, paving the way for more year-over-year vehicle sales.

Sam Fiorani

Source: Autocar